A Beginners Guide to Actuarial Mathematics

Copyright © 2025

INTRODUCTION

(an author’s note)

A warm welcome to “A Beginner’s Guide To Actuarial Mathematics”!

This book is created to introduce viewers to the captivating world of actuarial sciences. It is a branch that includes mathematics and focuses on managing risk and analyzing it as well. Actuaries are people who use mathematics, logical reasoning, and statistics to forecast the future and, in this way, help individuals, businesses, and governments to make appropriate and well-informed decisions.

Actuarial Science plays an important role in a lot of areas in today’s world. We see its presence in insurance, business planning, and healthcare. From predicting the disaster costs, calculating the expectancy of life, to setting premiums for insurance, actuaries make sure organizations stay stable and prepared for uncertainty in a very unpredictable world.

This guidebook was created for the purpose of making intricate ideas simpler and accessible. This book was created as part of the IB MYP Personal Project to help students become particular and recognize how mathematics may be applied beyond the classroom walls. I aspire to make actuarial concepts less intricate and to show how math can be fun and exciting!

Through the chapters ahead, we will be learning about the basic concepts of actuarial mathematics, which include statistics, probability, and risk assessment. We will also explore how these are used in real life.

This guide aims to construct a solid foundation for anyone interested in the career of actuarial sciences or for someone who wants to understand how math shapes the everyday decisions we take.

I hope this guidebook inspires you to look at mathematics as a powerful tool to making a safer future, and not just a subject!

CONTENTS:

CHAPTER 1: What is Actuarial Science? Pages 3 – 5

CHAPTER 2: The Actuarial Career Pages 6 – 9

CHAPTER 3: The Importance of Risk Pages 10 – 13

CHAPTER 4: The Mathematics Behind Actuarial Sciences Pages 14 – 19

CHAPTER 5: Actuarial Tools Pages 20 – 21

CHAPTER 6: The Future of Actuarial Sciences Pages 22

CONCLUSION Pages 23

REFERENCES Pages 24

CHAPTER 1:

WHAT IS ACTUARIAL SCIENCE?

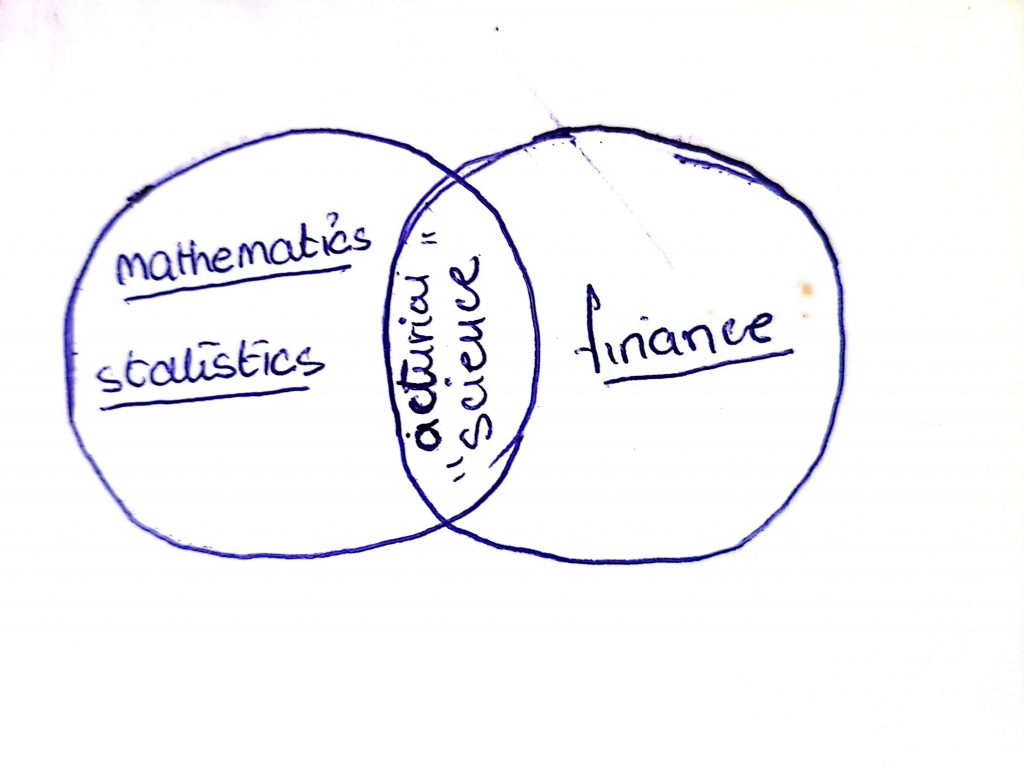

Actuarial science is the discipline that assesses financial risk in the insurance and finance fields by using mathematical and statistical methods.

It is the study of how mathematics and statistics can be used

to quantify risk. It helps individuals and companies make well-informed decisions about their futures. The people who are professionals in this field are called “Actuaries”. They are people who use models and numbers to forecast uncertain events such as losses (financial), accidents, & illnesses. (Society of Actuaries, 2020)

DEFINITION: Actuarial science, in simple terms, is the application of the study of mathematical topics such as statistics, probability, & general mathematics to predict uncertain events. Events especially with the involvement of money and risk. Actuaries then evaluate how likely these events are to happen, and what they would cost.

Let’s take a look at an example:

If an insurance company is seeking to learn how much they want to charge for their car insurance, this is where the role of actuaries comes in.

Actuaries then decide the ‘premium’ costs by first calculating the probability of the accidents, the age of the driver, or their experience, and then the repair costs. By looking at this data collectively, they set the prices of their insurance premiums to ensure that they are ‘fair’. This seeks to protect both the customer and the company.

![]()

ROLE OF ACTUARIES: The role of actuaries sets foot in both problem-solving and being analysts. To make sure uncertain situations have measurable results, they use mathematical models. Their primary job is to know how much the event would cost and how likely it may be to occur. Their areas of work would primarily be:

Reinsurance firms (helping insurers manage large risks)

Insurance Companies (predicting their losses and setting insurance premiums)

Pension funds (setting retirement payments)

Healthcare (evaluating medical costs)

Enterprise Risk Management (ERM) (pointing out and reducing risk in businesses)

They estimate the likelihood of future events.

They provide investment programs, insurance policies, and pension plans to help businesses in their financial planning.

They guarantee businesses to have sufficient funds to fulfill their commitments, such as claim payments.

They give advice to businesses on risk management and adherence to financial rules and regulations.

Why is Actuarial Science important?

Actuarial science is important in today’s world. It helps individuals, companies, businesses, and governments to prepare for uncertain events and make those situations into being manageable.

Businesses would struggle to manage risk, the government would not know how to plan for pensions, and companies would struggle to set fair prices without actuarial science.

If we look at it from the aspect of everyday life, we see that it brings stability and fairness in our lives. It builds the bridge of trust between consumers and producers, and protects societies from financial risks by quantifying them and identifying them beforehand.

How does Actuarial Science incorporate mathematics, statistics, and finance together?

The 3 main pillars that actuarial science is built upon are:

- Finance: to be able to understand how money converts to value over time, to be able to make certain financial decisions.

- Mathematics: used for modeling, calculations, and problem-solving, etc.

- Statistics: to be able to understand patterns and analyze data.

But how? Let’ take a look at some examples:

By using the mathematical concept of ‘probability’, they can calculate the chance of a person living beyond the age of 80+ years.

Then they use financial formulas to control how much money should be laid aside for the payment of that person’s pension.

And then they may use statistics to ensure the accuracy and study larger groups of people.

Let’s look at an example to clear all this up:

So let’s imagine an insurance company is setting up healthcare insurance for 1,000 people.

If data shows that on average, only 50 people will need expensive hospital treatment costing around $5,000, then actuaries may estimate:

50 X $5,000 = $250,000 (their annual costs)

The company then succeeds in spreading this healthcare premium across 1,000 people and adds a small profit margin as well as a safety margin. This is how the company makes sure that everyone pays fairly for their premiums and that the company stays secure, financially.

CHAPTER 2:

THE ACTUARIAL CAREER

Intro:

Actuarial science is a profession. They are the people who turn theories into decisions. They do that by the use of numbers, data, and logic to help individuals, companies, and governments manage their risks and predict the future. Becoming an actuary is one of the most rewarding and respected careers in the world, as it combines the use of intelligence, problem-solving, and precision, and it creates a real impact.

Actuaries:

Actuaries can be called ‘fortune tellers’ of finance; they can guess as well as predict the future by using logic and mathematics.

Actuaries are ‘specialists’ when analyzing and predicting uncertainty. They study and as well as build data & models. To help organizations make safe decisions and make sure they’re profitable, they help calculate probabilities.

E.g.

They calculate how likely the incident of a car accident is – how long is it that people live after retirement – how much money should any insurance company lay aside for future claims?

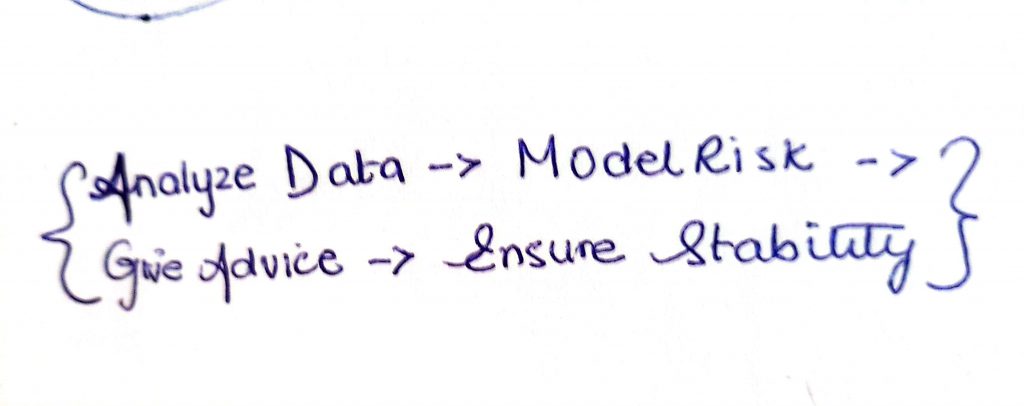

The Roles & Responsibilities of an Actuary:

Actuaries are the people who protect companies and individuals from financial losses, and help them stay financially stable. They help them plan for uncertainty. Their responsibilities include;

- Advising companies and individuals for financial planning

- Clearly communicating their results for their non-mathematical audiences.

- Designing and pricing insurance premiums & pension plans

- Analyzing data and identifying risks.

- Estimating financial costs of future events.

(Institute and Faculty of Actuaries, 2021)

Areas of Work:

Actuaries take place in a wide variety of work industries, they can take place in offices, firms, and government departments.

- Pensions – Planning retirement funds

- Healthcare – They evaluate medical costs and risks

- Government – Public policies & social programmes

- Insurance – Claim probabilities & premiums

- Finance & Investment – Helping with financial portfolios

- Reinsurance & ERM – Manage large-scale risks

They also deal with global organizations & help them with long-term planning and their risk management on a global scale as well.

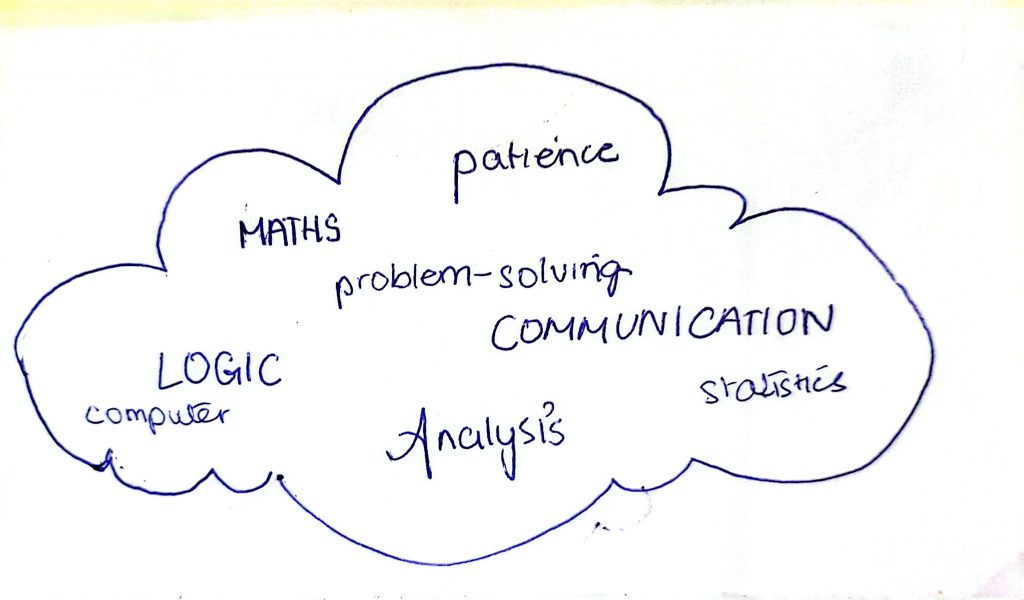

Actuarial Skills:

To be able to succeed and climb in this career, you need to possess the following skills, whether they are technical or personal;

- Analytical thinking – Understand complex problems

- Decision making & Problem solving – Being able to give advice confidently

- Patience – Problems can take time to solve

- Mathematical skills and Statistical skills – Analyzing data and being able to build models

- Communication skills – Explaining results clearly

- Computer skills – Being able to use software

EXAMS & Qualifications:

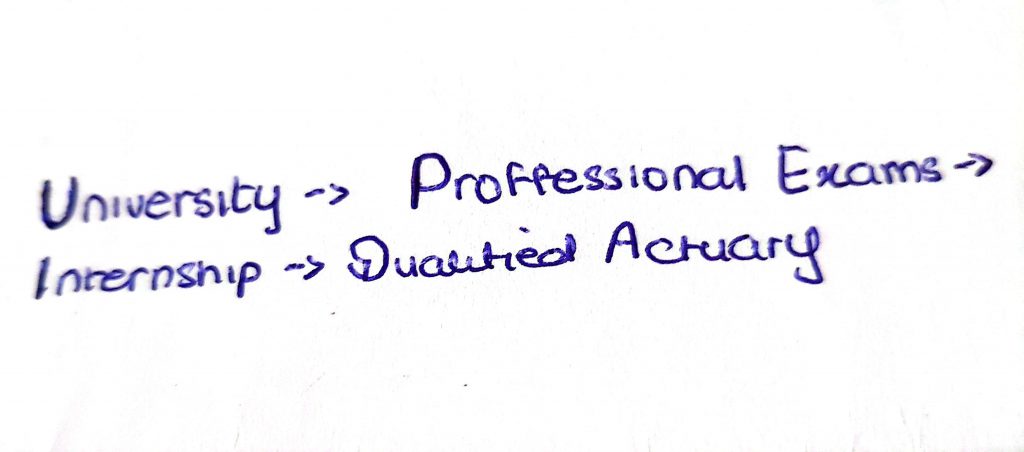

Becoming a certified actuary takes time and patience. This includes passing exams and qualifications recognized by bodies such as:

The Society of Actuaries (SOA) – in the US

The Institute and Faculty of Actuaries (IFoA) – in the UK

The Institute of Actuaries of Pakistan (IAP) – in Pakistan

(Society of Actuaries, 2022)

These exams build knowledge step-by-step, and once you are qualified, you earn the title of ‘Fellow’ and which shows you are an expert in the field.

The exams cover vast topics such as Financial Mathematics, Probability, Economics, and risk management. It can take up to 5-7 years to be properly qualified, and students take these exams during or after their university studies. Actuaries can also start working and gaining experience while studying.

Career & Growth Opportunities:

The actuarial career has excellent growth opportunities and you can climb very high. You can move into senior positions and roles such as :

Actuarial consultant

Reinsurance specialist

Risk Manager

Chief Risk Officer

Investment Analyst

Across the entire globe, actuaries are in high demand, because they are in every industry that deals with risk and uncertainty, and that makes this entire profession stable and also well-paying. They have their unique ability to understand both business and numbers.

Conclusion:

So, in conclusion.

An actuary does not just work with numbers, but also works with organizations and helps people prepare & and create a stable future.

They play vital roles in today’s uncertain world and use data to make confident and well-informed decisions. It can be a career for those who enjoy mathematics, learning continuously, and problem-solving.

If you enjoy mathematics, solving real-world problems, & discovering patterns, this may just be the career path for you!

“Actuaries don’t just predict the future, they certainly prepare for it.”

CHAPTER 3:

THE IMPORTANCE OF RISK

What is Risk?

Any event that could lead to repercussions or losses, and the chances of that happening are called risk. Risk does not mean it could always be something bad, but it is more towards the uncertainty of the outcome. (Harrington & Neiheart, 2004)

Let’s take the stock market as an example. When you invest in the stock market, you know that you have the potential ‘risk’ of losing money, and also the possibility of gaining it.

So in order to make smart decisions, actuaries use data and analyze & measure these chances to make well-informed and smart decisions.

To give an example – If it is in the knowledge of the actuary that every year 1 out of 100 houses gets damaged from flood, this is how they can set insurance premiums fairly & protect the homeowners as well as the company.

Risk in Actuarial Sciences:

Risk is embedded in the heart of actuarial science. If there were no risk, actuaries would not be needed.

Risk – the possibility of an unexpected event occurring in the future. Risk takes place everywhere – from healthcare to business and finance. Even the choices we make daily are full of risk.

Actuaries study this risk to make sure that there are fewer chances for uncertainty. They help individuals and organizations by predicting what might happen. So when these events do occur, the individuals and organizations know how to handle the effects.

Types of Risk:

Actuaries are responsible for studying various types of risks. All of these risks affect different types of people in varying ways. To make sure that their impact is reduced, actuaries study & understand all of them.

Various risks may include;

- Insurance Risk – Accidents, problems, or disasters.

- Mortality & Longevity Risk – life insurance, how long people live.

- Operational Risk – Failures, human errors, and mismanagement.

- Financial Risk – Market changes, investment, interest.

- Business & Credit Risk – Cannot pay back loans/money

- Catastrophic Risk – severe events (earthquake, pandemics)

WHY is Risk important in Actuarial Sciences?

Risk has its effects on everything, and this is why actuaries must turn the “uncertainty” of this risk into information that can be measurable so that individuals and companies can make well-informed and confident decisions.

Businesses would have no way to plan for losses, accidents, or changes in the market, if there were no actuaries. So when actuaries study risk, they are helping;

- Set pension funds – (long-term stability)

- Helping businesses reduce their losses

- Insurance companies set prices

- Help governments prepare social programmes & healthcare

As far as mathematics allows, actuaries “predict the unpredictable”.

How do actuaries calculate risk?

To measure how much the data varies from the mean, actuaries use Expected Value (EV).

EV is the weighted average of outcomes, and it is used to set insurance prices, and then actuaries decide how much to charge.

Expected value is a way to find the average cost of a risk over time. They calculate the average result from all possible outcomes that may happen.

The formula for EV:

EV=∑(Probability × Outcome)

(chance of outcome 1 x value of outcome 1) + (chance of outcome 2 x value of outcome 2)

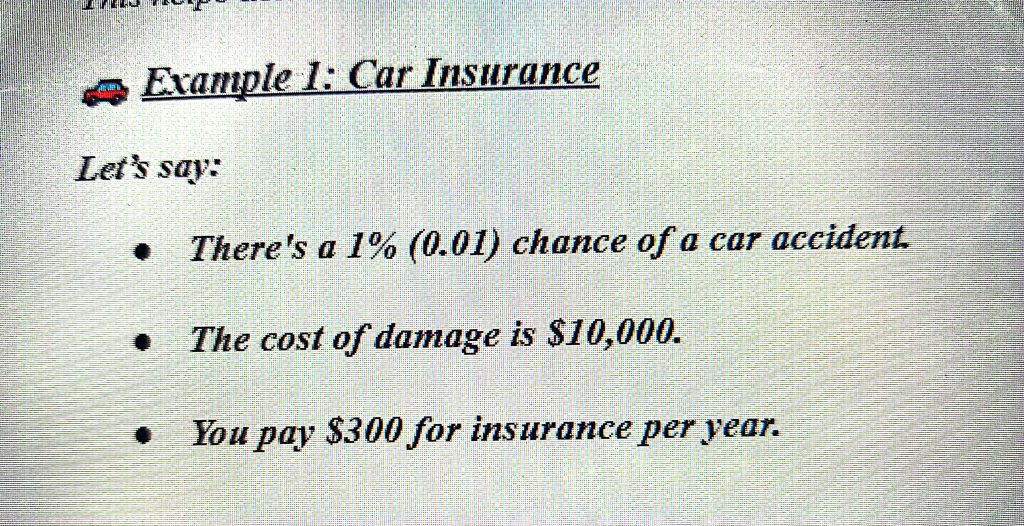

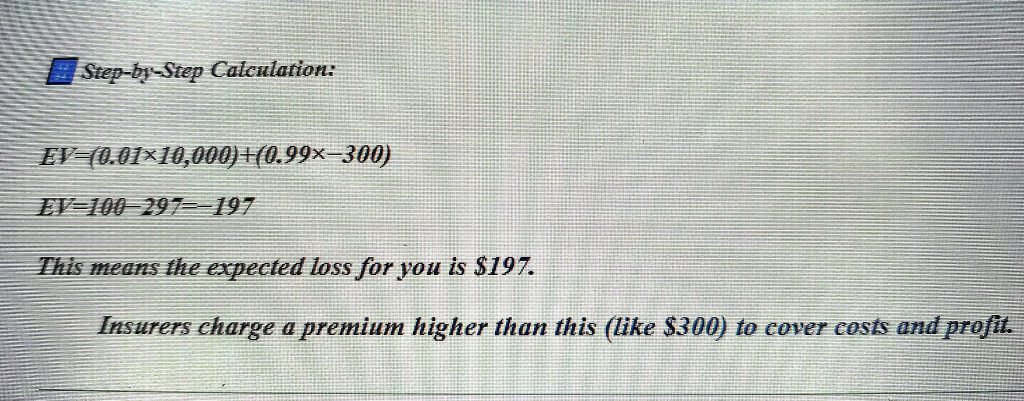

An example for EV can be:

Risk as a concept in real life:

Risk is a part of your everyday life. If we look into our daily lives, we take small risks here and there. For example, today I risked my life by crossing the road, or I invested money here, or even while choosing a career.

To make those risks manageable, actuaries predict beforehand and then expect the solutions in advance, so that nothing goes wrong.

If we take a look at real-life examples, we see that;

Pensions: They calculate how much money a person should save to live comfortably after retirement.

Car insurance: They calculate the likelihood of accidents and determine fair prices for drivers based on this assessment.

Health Insurance: To keep hospital patients protected, they calculate the likelihood of illnesses and set premiums accordingly.

This is how actuaries build strength, trust, and fairness in modern society.

In Conclusion, risk is important for actuaries to study, because risk is everywhere in our lives. Actuaries help make our world predictable and much safer, and show that we can prepare, study for, and measure risk so that we can prepare for uncertainty.

Through actuarial science, we can turn risk into knowledge, and this is why it is one of the world’s most complex and valuable careers today.

CHAPTER 4:

THE MATHEMATICS BEHIND ACTUARIAL SCIENCES

Actuarial sciences stand upon the foundation of mathematics. An actuary doesn’t make any decisions without mathematical principles and calculations. They use mathematical principles such as statistics, probability, and financial mathematics to measure risk, analyze data, & predict future events.

This chapter is largely based on the basic mathematical principles that actuaries rely on, which include variability, averages, standard deviation, and the law of large numbers. They will be explained in an easy-to-understand way.

Basics of probability:

The study of how likely something will occur is the study of probability. To estimate the future, actuaries use this probability for events such as illnesses, fatalities, accidents, and deaths. (Ross, 2014)

If the occurrence is impossible, then the chance for that event is 0.

If the chance is 1, then the event is certain.

Anything else in between is the ‘degree of chance’.

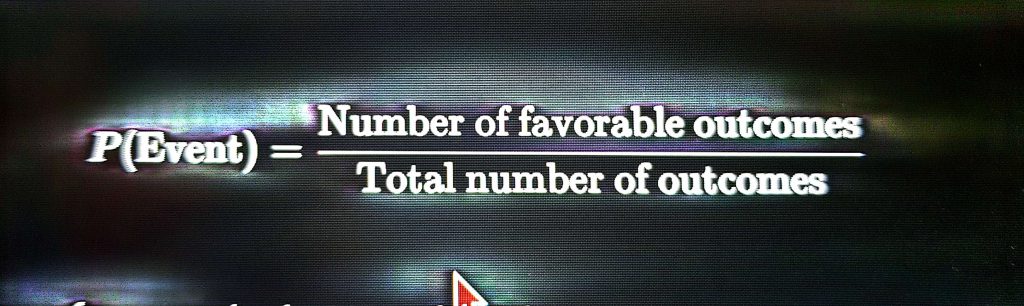

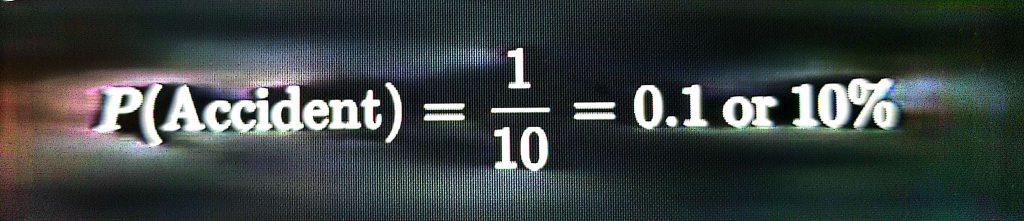

Formula for Probability:

Example:

If the chance of a person having an accident is 1 in 10 in a year, then;

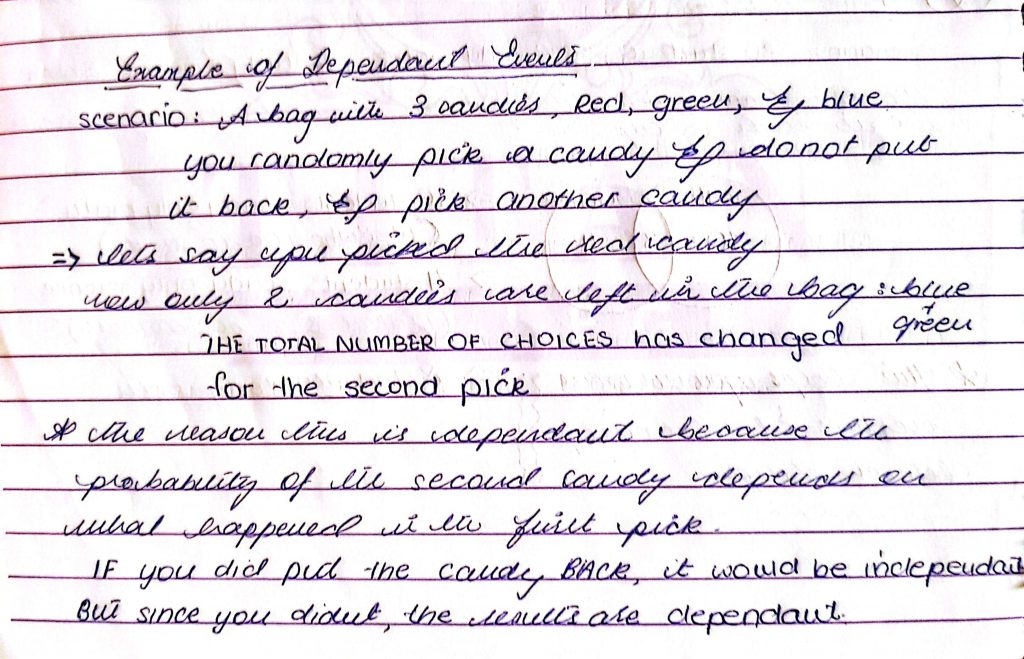

Independent and dependent events:

If one event’s outcome has no bearing on the other events’ outcome, then the events are independent.

A good example can be when we throw a coin.

The result of throwing one coin has no bearing on the other. This means that the events are independent.

“P(A and B)=P(A)×P(B)”

Now you can derive what dependent events are.

When the outcome of one event relies on or “influences” the other, then the events are dependent.

For eg, If you draw 2 cards from a deck, and don’t swap out the first one, then what was taken first determines the second draw.

“P(A then B)=P(A) × P(B|A)”

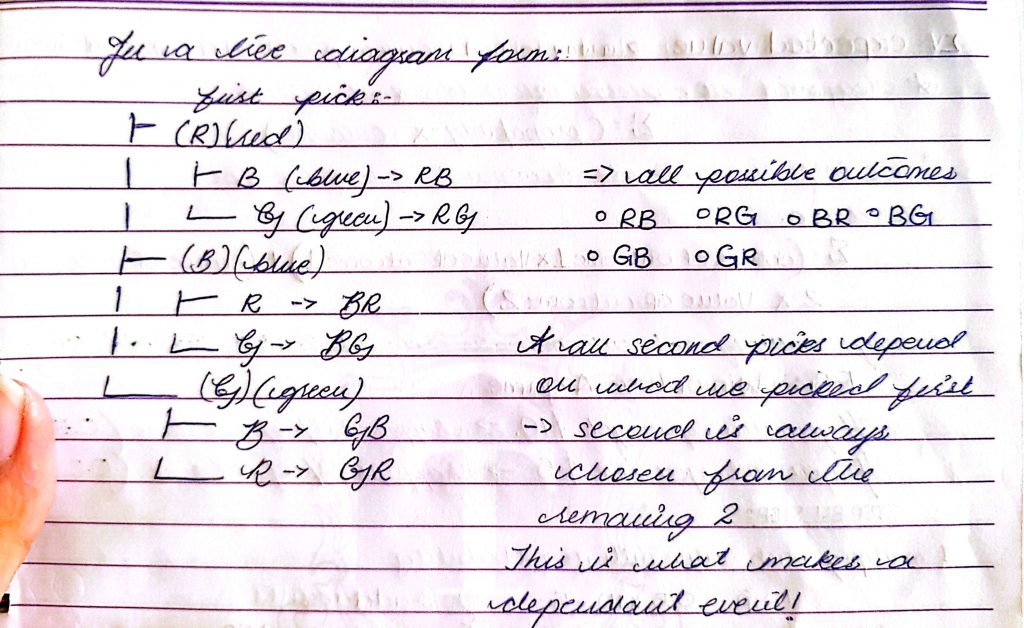

Hopefully, this visual helps make it easier (it also includes tree diagrams, a topic further ahead):

Examples from real life:

Games: determining the results of rolling a dice or spinning a wheel, probability is used.

Medical testing:

Insurance: Actuaries estimate the likelihood of illnesses, fatalities, or mishaps to determine the costs of policies.

Weather forecasting: The probability of rain is 70%, according to the forecast.

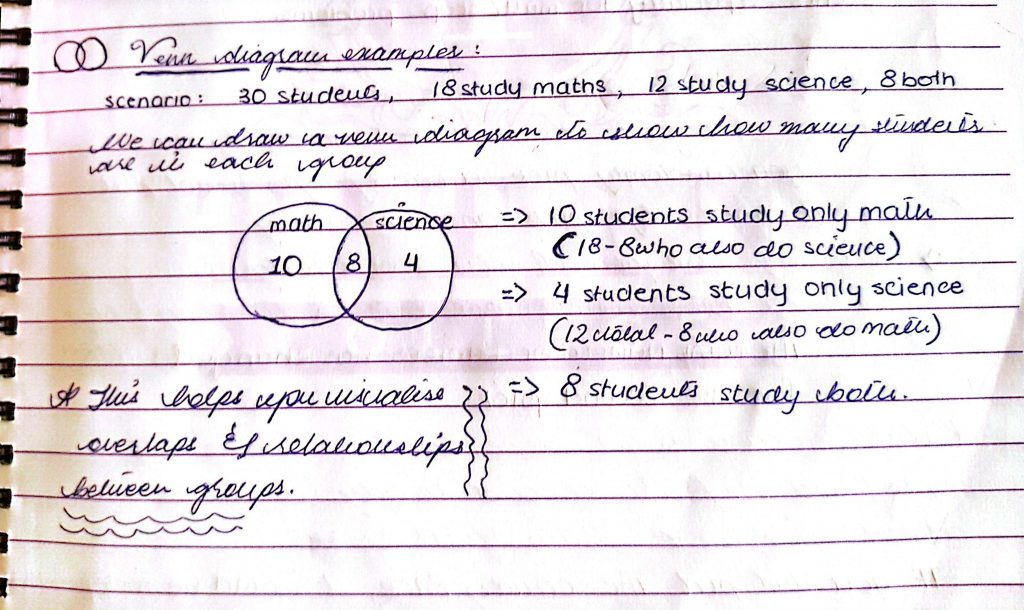

Venn & tree diagrams:

Venn diagrams are used to describe overlapping events, and they are useful for understanding events that are mixed, mutual, or exclusive.

Here is a visual to help clarify:

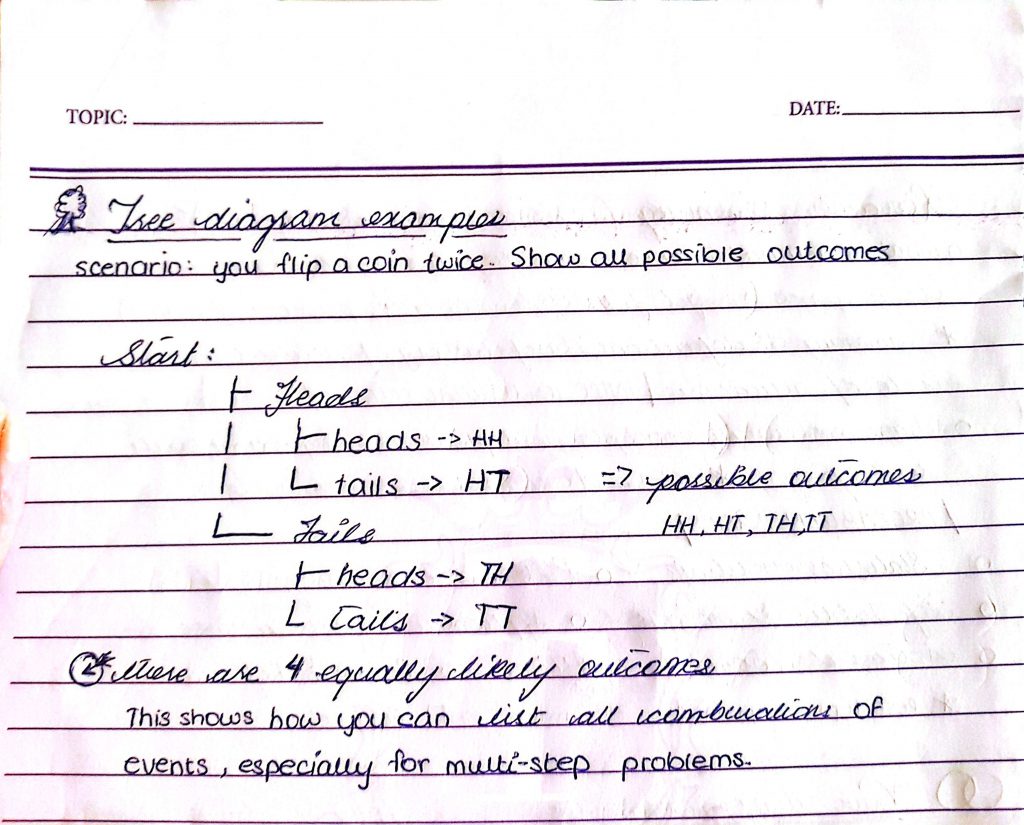

Tree diagrams provide a step-by-step list of all possible outcomes. They are great for explaining situations that have multiple steps, such as ‘flipping a coin’. These diagrams also make independent and dependent events easier to look at.

Here is a visual to clarify and help you understand:

Basics of statistics:

Whilst probability is the study of an event occurring, statistics is studying what has already happened. Actuaries do this by analyzing data, preferably large amounts of data in order to predict the future.

Key statistical terms:

Some key statistical terms include:

Mean: The mean is the average, meaning it is the sum of all the values, divided by the number of values.

📌 Example:

60, 70, 80

→ (60 + 70 + 80) ÷ 3 = 70

Median: When the numbers are arranged in order, the middle value is known as ‘the median’

📌 Example:

60, 70, 80

→ 70 is the middle

📌 If even numbers:

60, 70, 80, 90

→ Median = (70 + 80) ÷ 2 = 75

Mode: The most repetitive number.

📌 Example:

60, 70, 70, 80

→ 70 is the mode (it comes twice)

A collective example would include:

The number of car accidents yearly for 5 people: 3, 2,5,2,8

Mean:(3 + 2 + 5 + 2 + 8)= 20 ÷ 5 = 4

Median: 3 (middle value in correct order 2, 2, 3, 5, 8)

Mode: 2 (most repetitive)

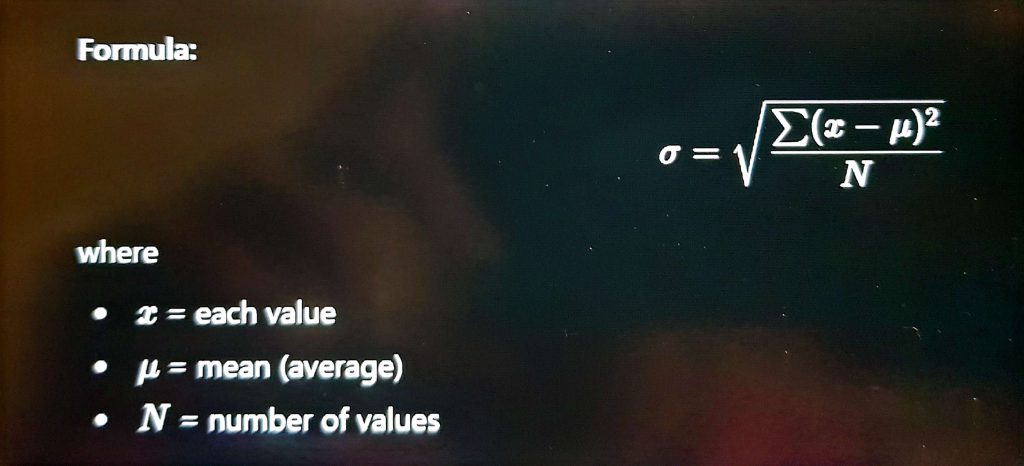

Standard Deviation (Variability):

Even though taking out the average is important, actuaries also study how spread out the data might be. To do this, actuaries use ‘variability’.

If the different values are closer to the ‘average’, there is ‘low variability’, and if the values are far apart, then there is ‘high variability’.

Now, to do this, they use ‘standard deviation’.

What is standard deviation?

Standard deviation is the spread of numbers.

Let’s take an example:

Here are the ages of people who are insured: 30, 31, 29, 28, 30, 30.

Here, the numbers are close together, meaning that the standard deviation is ‘low’ or ‘small’. This results in low risk and variation.

Another example: 25, 45, 35, 55, 60.

Here we see that the numbers are pretty far apart. Therefore, the deviation is higher, meaning a greater chance of uncertainty and variety in the group.

To find the SD, they use this formula:

So, in sum up;

If the SD is low, the numbers are close

If the SD is high, numbers are far apart.

📌 Example:

80, 81, 82 → Low

50, 80, 100 → High

Data Interpretation:

An Actuary’s job is to understand what the numbers or graphs are saying. They look at the data and then see what it means.

For example:

There is a list of the monthly car accidents for the following months:

June: 20

July: 40

August: 70

August, you see, has the most accidents, so by looking at this, what is an actuary’s job? An actuary’s job is to look at this data and say, “March seems risky; perhaps we should charge more for insurance in March!”

Real-World Use in Actuarial Models:

Actuaries then use these ‘statistics’ in industries such as;

Retirement Planning:

They study how long people live (life expectancy) and how much money an average person needs after retiring. (using median and average)

Health Insurance:

They study how many people get sick at certain ages & how much the hospital charges them. (using mean, standard deviation, and graphs)

Car Insurance:

They study how many accidents happen in each area and during which time of the year the accidents increase. (using bar graphs and pie charts)

“The Law of Large Numbers”:

In the field of actuarial science, there is a thing called ‘the law of large numbers’, which is very important. The law states that the more data you study and collect, the more valid your predictions are. (Grimmet & Welsh, 2014)

So when actuaries observe, as the number of observations increases, their predictions and results become more accurate relative to the actual results.

E.g., if an actuary states (predicts) that out of 100 people, 1 person will have an accident, and he tests this statement with only 10 people, his results may be inaccurate.

But instead, if he tests this statement with around 10,000 people, his results may be more valid and closer to the prediction he made.

Since larger groups make for more accurate data, insurance companies rely on heavier and big data.

How do Actuaries Predict these events?:

Actuaries create mathematical models by combining probability and statistics. These models then predict the likelihood of events and the financial effects they would have.

They study:

Financial Values: They measure the coming financial losses.

Probabilities: They predict outcomes and the likelihood of events occurring.

Past Data: They understand the patterns and trends of the past.

A good example to help clear this up would be:

The probability of a person filing a claim for health insurance in a year is 5%. The cost of the claim would be $2000.

The expected cost per person would then be found like this:

0.05 x 2000 = $100

This calculation shows us that the amount that the company should charge is $100 for their premiums (alongside a margin) for a person to stay financially stable.

In conclusion, why do these concepts matter?

Actuarial science is the reason we know why mathematics is much more than just numbers and calculations. It is how they understand uncertainty and how they bring it into being confident.

These concepts, if shown one by one:

Probability: “predicting what might happen”

Standard Deviation: “how unpredictable a situation is”

Statistics: “what has happened”

The Law of Large Numbers: “ensuring accuracy”

Through this entire chapter, we have learnt how important mathematics is in every actuarial decision. They help turn complex and unpredictable situations into manageable and clear events. It is the foundation of actuarial science.

![]()

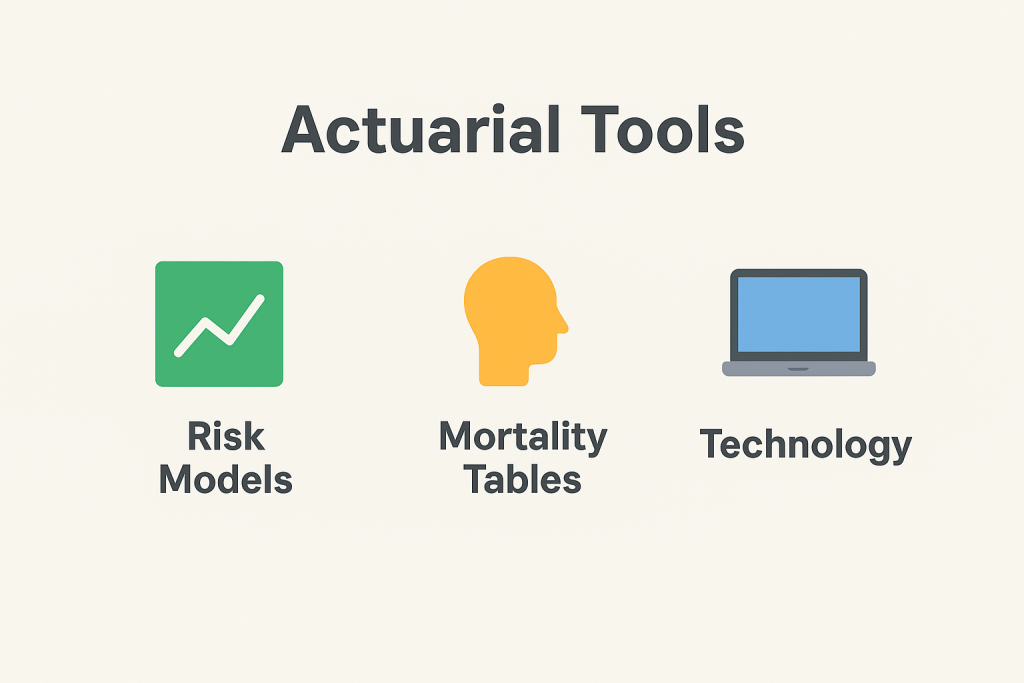

CHAPTER 5:

ACTUARIAL TOOLS

Actuaries use many different tools to turn their data into results that are meaningful. These tools, in turn, help actuaries communicate their complex results clearly, analyze & quantify risk, and make predictions.

This chapter will be divided into 3 main sections, which include actuarial tools. They are as follows:

1. Mortality Tables

2. Risk Models

3. Technology

These are key features that enable actuarial work.

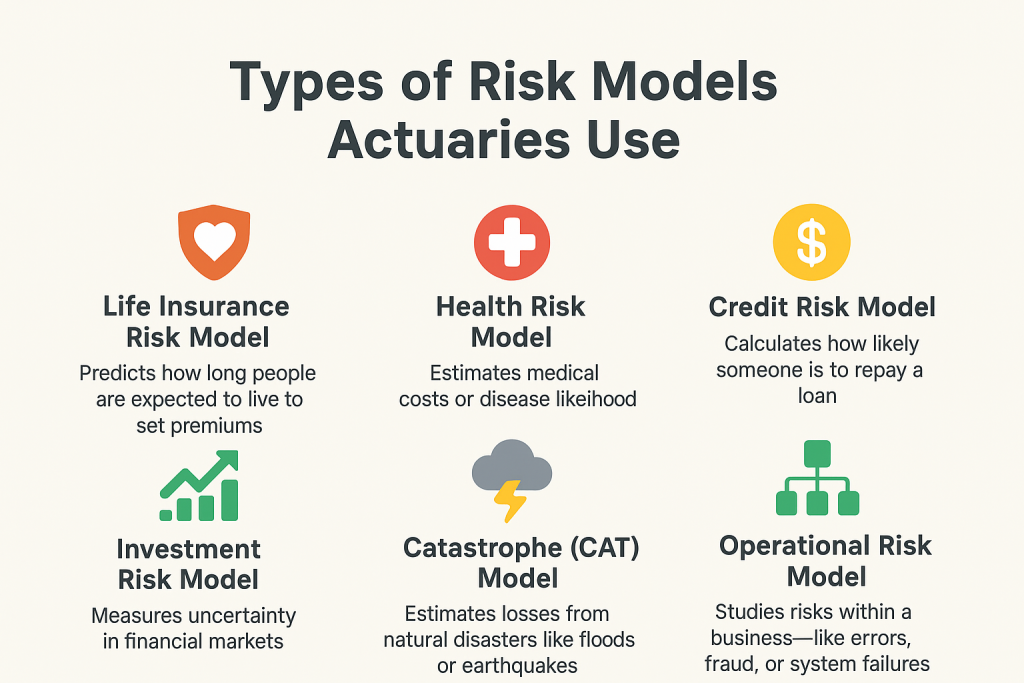

RISK MODELS – PREDICTING FINANCIAL OUTCOMES:

To estimate the likelihood of future events and their financial outcomes, actuaries make risk models. It could be called ‘the mathematical representation of reality’, and it helps clear concepts such as:

“How likely is a person to have an accident this year?”

“What are the expected costs in a company for their medical claims?”

These ‘risk models’ clear up the ‘what if?’ situations for an actuary by using statistics, probability, and financial data. There are different models for different situations. They could use a ‘loss model’ to determine how much they may have to pay in claims after a storm hits, or a ‘credit risk model’ to know how a borrower may be likely to default on their loan.

A simple example would be an Insurance Risk Model:

An Insurance company does not know how much to charge for its car insurance. To be able to know that, they need to predict the ‘risk’ of these car accidents and how likely they are to occur.

The risk model works like:

- The company first collects data, e.g., driving experience, age, car type, history of accidents, etc.

- They then use formulas from math’s and statistics to know the probability of the driver being in an accident.

- Lastly, they find out the expected cost and set the insurance premium

Formula for ‘expected cost’:

A simple example calculation:

The probability of an accident: 0.05 (5%)

The cost of an accident on average: $10,000

Using the formula:

EXPECTED COST: 0.05 x $10,000 = $500

So the company can charge $500 per year + keeping a profit margin and expense margin.

This matters because it ensures that insurance companies stay financially stable and also make sure that customers pay fair prices according to their level of risk.

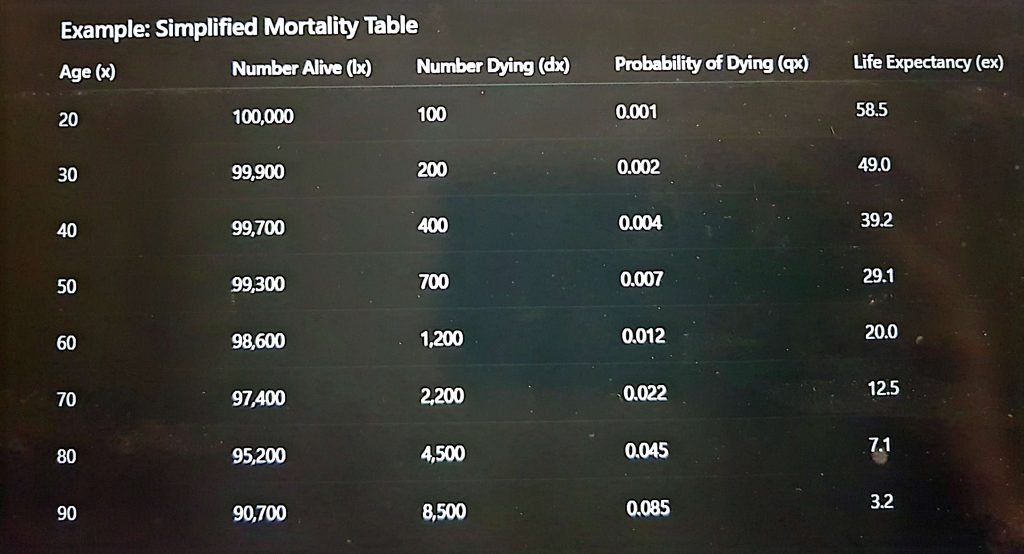

MORTALITY TABLES – Life Expectancy

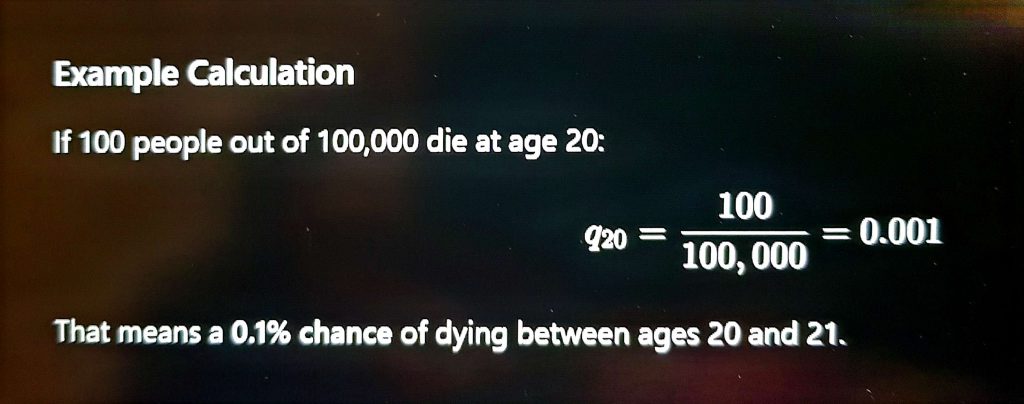

Another essential actuarial tool is called the ‘mortality table’, also known as the ‘life table’.

A life table is like a chart that tells us:

- At each age, how many people are still alive

2. What chance a person has to live or die in the next year

It is an essential tool for actuaries, as it enables them to calculate the probability of a person of a certain age dying before their next birthday. This helps them know how, on an average basis, a person is expected to live.

These tables are important to an actuary, as they help them:

- Calculate premiums for life insurance based on life expectancy

- Calculate how long the payments will need to continue for pensions

- Calculate long-term medical costs for healthcare

Here is a simplified mortality table example:

Explanation:

The Age(x) is the age group of people

The Number Alive (lx) is the number of people who are alive at that age out of the 100,000 sample number.

The Number Dying (dx) is the people who die before reaching the next age

The Probability of Dying (qx) is the chance of dying between the current age and the next.

The final Life Expectancy (ex) is the number of years they are still expected to live.

An example calculation for you to understand better:

TECHNOLOGY – A TOOLKIT FOR A MODERN ACTUARY:

In today’s modern and quickly advancing world, actuaries rely heavily on technology for handling large amounts of data, and for performing difficult calculations much quicker and efficiently.

They use many modern tools, and they include:

-

Microsoft excel

Excel sheets are used for data analysis, financial modeling, and spreadsheets. This is the base ground for actuaries, and this is where they start to learn how to work with data.

This is what a spreadsheet of columns may look like on excel:

Age | Probability of Death | Expected Value | Premium

25 | 0.001 | $200,000 | $200

35 | 0.002 | $200,000 | $400

2. Python

Python is a powerful programming language that is used to analyze large sets of data, make visualizations, and automate processes. It is quite popular for predictive modeling and machine learning.

3. R

R is a programming language that is used for data visualization and statistics. It helps graphs explain their results clearly and run advanced statistical models.

4. Actuarial Software

There are some professional and paid software that actuaries use in insurance companies for complex financial modeling and regulatory reporting systems. These are paid tools. They can be tools such as Prophet, AXIS, & MoSes.

In conclusion, these technologies make actuarial work faster and much more precise, and this allows actuaries to interpret the data and not focus a large portion of their time on calculating it.

So behind every pension plan, insurance premium, and financial forecast is the careful work of an actuary. They transform this data into protection for millions of people around the globe.

CHAPTER 6:

THE FUTURE OF ACTUARIAL SCIENCES

The world is at an ever-faster pace, and new kinds of data, technology, and risk are transforming how businesses manage themselves. This proves that actuarial science is evolving as well, and in the future, actuaries will play an even heavier role in understanding this new risk and predicting events. This will help organizations make smart and accurate decisions.

DEMAND FOR ACTUARIES:

As the world continues to grow, actuaries become ever more in demand and valuable across the globe. As countries develop their insurance sectors and their financial systems, they need professionals who can quantify their risk and manage it.

To handle their long-term climate, insurance pricing, and health planning, global organizations such as Europe, Asia, Africa, and North America are expanding their actuarial teams.

This career is recognized as one of the most well-paying and stable professions, and it provides opportunities in the private and public sectors.

As long as uncertainty grows, there will always be a need for actuaries.

EMERGING FIELDS FOR ACTUARIES:

As the world is growing, actuaries are now entering fields that they didn’t a few decades ago. These new fields include:

- 🌎Climate & Environmental Risk: As climate change is a growing global concern, actuaries study this environmental data and the losses from natural disasters to help governments and businesses plan for their future.

- 💻Cyber Risk & Technology Insurance: As the world grows, cyberattacks and data breaches become another growing risk for modern companies. Actuaries use models to detect the financial losses from these events & this creates kind of a ‘digital insurance’.

- 🧠Artificial Intelligence (AI) & Machine Learning: Actuaries are now adapting to the fast-changing world and creating models to predict their customer behavior, optimize their investment strategies and to be able to detect fraud.

- 🏥Healthcare and Biotechnology: As the advancements in medical technology continue to grow, actuaries assess the costs of these new benefits and their new treatments. They also predict health trends of the population and create the way for new & advanced healthcare systems.

- 📉ERM (Enterprise Risk Management): Businesses now want full views of their potential risks, not just financial, but their overall reputational risk and their operational risk as well. This is why ERM continues, and actuaries are the foundation in this field.

(Deloitte, 2020)

Why Actuaries WILL remain important:

🌎As the world grows, artificial intelligence takes the computerized tasks, but even then, actuaries are the ones who will bring judgment. They will bring the context to decision-making. This is something no machine or AI can ever replace.

An actuary’s primary job is not to just calculate numbers. Actuaries interpret these numbers to make decisions. As the world grows, so does uncertainty, and to be able to understand this uncertainty is how actuaries keep governments and businesses stable. So regardless of how advanced technology gets, actuaries will be essential in every era, because of their business understanding, their mathematical expertise, and their analytical thinking.

SKILLS:

Future actuaries will need to develop more than just mathematical skills to stay ahead in their field and in this changing world. Those actuaries who will be the most successful will possess skills such as:

Being ethically aware (making sure that fairness and transparency is inculcated in financial systems)

Being creative problem solvers (they must be able to think beyond just numbers)

Being strong communicators (they must be able to explain complicated concepts to non-skilled people)

Being technologically skilled (they should be comfortable with visualization tools |chapter 5|)

CONCLUSION

In this guidebook, we have explored the diverse world of actuarial sciences. It is not just a field of numbers, but it is a field that puts knowledge into protecting people and their futures.

The importance of actuarial science will grow as the world advances. Actuaries will continue to bridge the gap between uncertainty and the real world. Actuaries play a vital role in today’s world, from bringing safety to our homes to bringing stability to the global markets.

To any students who are interested in this field, actuarial science is not as intimidating as it seems, it is only about persistence, curiosity & creativity. If you are a person who enjoys working with data, solving problems, and try to make an impact with logic, then this path is determined for you!

It takes serious dedication to become an actuary. But once you reach the goal, it is a career worth the reward. It comes with the promises of stability, purpose, and growth. I truly hope this guidebook has inspired you to explore the world of actuarial science, and to see how meaningful this career truly is.

After all, “in a world full of uncertainty, actuaries are the ones who turn this doubt into direction. Numbers can tell stories, but actuaries are their translators.”

References:-

Kagan, J. (2023, September 28). What is actuarial Science? Definition and Examples of application. Investopedia. https://www.investopedia.com/terms/a/actuarial-science.asp?utm

Morgan State University. (n.d.). What is actuarial science? Retrieved June 5, 2025, from https://www.morgan.edu/actuarial-science/prospective-students/what-is-actuarial-science

Actuarial Careers. (n.d.). Areas of work. Retrieved June 5, 2025, from https://www.actuarialcareers.co.uk/profession-overview/areas-of-work/

University of California Riverside, School of Business. (n.d.). Actuarial science. Retrieved June 5, 2025, from https://business.ucr.edu/undergraduate/actuarial-science

ProActuary. (n.d.). What does an actuary do? Retrieved June 5, 2025, from https://proactuary.com/resources/what-does-an-actuary-do/

JCW Resourcing. (n.d.). Actuarial jobs: An overview of the career path and job opportunities. Retrieved June 5, 2025, from https://www.jcwresourcing.com/insights/blog/actuarial-jobs–an-overview-of-the-career-path-and-job-opportunities/

Investopedia. (n.d.). Probability. Retrieved June 10, 2025, from https://www.investopedia.com/terms/p/probability.asp

Khan Academy. (n.d.). Probability and statistics. Retrieved June 10, 2025, from https://www.khanacademy.org/math/statistics-probability

GeeksforGeeks. (2025, March). Dependent and independent events in probability. Retrieved June 18, 2025, from https://www.geeksforgeeks.org (geeksforgeeks.org)

Investopedia. (n.d.). What is standard deviation? Retrieved June 18, 2025, from https://www.investopedia.com (analystprep.com)

Statology. (2021, March). Real-life examples of mean, median & mode. Retrieved June 18, 2025, from https://www.statology.org (statology.org)

Robidoux, B. (2024). Expectations, probability and uncertainty. The Actuary Magazine. Retrieved from https://theactuarymagazine.org

Vaia Learning. (n.d.). Expected Value in Insurance and Risk. Retrieved from https://www.vaia.com

Investopedia. (2023). Insurance Premium. Retrieved from https://www.investopedia.com/terms/i/insurance-premium.asp

Life Expectancy Project. (n.d.). Life table basics. Retrieved from https://www.lifeexpectancy.org/lifetable.shtml

Society of Actuaries. (2023). Actuary Career Paths. https://www.soa.org/resources/career/paths

Published: Nov 30, 2025

Latest Revision: Nov 30, 2025

Ourboox Unique Identifier: OB-1694320

Copyright © 2025

![]()

Skip to content

Skip to content